Comprehending VA Home Loans: A Comprehensive Overview for Armed Force Households

Comprehending VA Home Loans: A Comprehensive Overview for Armed Force Households

Blog Article

Navigating the Home Loans Landscape: How to Leverage Financing Solutions for Long-Term Wide Range Structure and Protection

Browsing the intricacies of home fundings is essential for anybody looking to construct wealth and ensure financial safety. Recognizing the different kinds of financing options offered, along with a clear evaluation of one's economic situation, lays the foundation for informed decision-making.

Understanding Mortgage Types

Mortgage, a vital part of the realty market, been available in different kinds created to fulfill the varied requirements of customers. The most typical kinds of home mortgage consist of fixed-rate home mortgages, variable-rate mortgages (ARMs), and government-backed loans such as FHA and VA lendings.

Fixed-rate mortgages use security with regular month-to-month settlements throughout the financing term, generally varying from 15 to three decades. This predictability makes them a preferred option for novice property buyers. On the other hand, ARMs include rate of interest that fluctuate based on market problems, commonly causing lower first repayments. Debtors need to be prepared for potential increases in their monthly obligations over time.

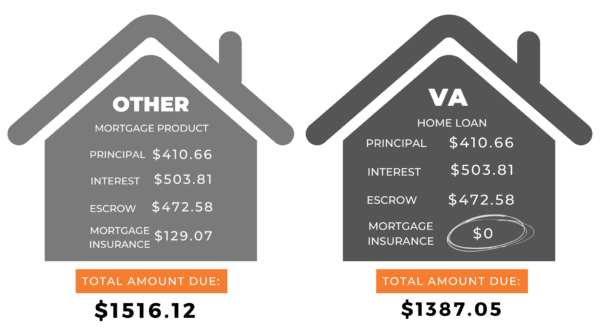

Government-backed loans, such as those guaranteed by the Federal Real Estate Management (FHA) or ensured by the Department of Veterans Affairs (VA), satisfy certain teams and often call for reduced down repayments. These car loans can help with homeownership for people who might not qualify for traditional financing.

Analyzing Your Financial Scenario

Reviewing your economic scenario is an essential action in the home loan process, as it lays the structure for making educated borrowing decisions. Begin by assessing your income sources, including incomes, incentives, and any kind of extra profits streams such as rental homes or financial investments. This extensive view of your earnings aids lenders determine your loaning capability.

Next, analyze your costs and month-to-month obligations, consisting of existing financial debts such as charge card, student lendings, and auto settlements. A clear understanding of your debt-to-income ratio is vital, as a lot of loan providers prefer a proportion below 43%, ensuring you can take care of the new mortgage repayments alongside your current commitments.

Furthermore, review your credit rating, which considerably impacts your lending terms and passion rates. A greater credit history shows financial dependability, while a reduced rating may demand strategies for enhancement prior to making an application for a funding.

Lastly, consider your cost savings and properties, consisting of reserve and liquid financial investments, to ensure you can cover down settlements and closing expenses. By diligently assessing these parts, you will be much better placed to browse the mortgage landscape successfully and protect funding that aligns with your lasting economic objectives.

Strategies for Smart Borrowing

Smart loaning is important for navigating the intricacies of the home financing market properly. A solid debt rating can substantially decrease your passion rates, translating to significant financial savings over the life of the loan.

Next, consider the sort of mortgage that best matches your financial situation. Fixed-rate finances offer stability, while adjustable-rate home loans may offer lower preliminary repayments however carry risks of future rate increases (VA Home Loans). Assessing your long-lasting plans and financial ability is important in making this decision

Additionally, aim to safeguard pre-approval from lending institutions before residence useful reference hunting. This not only offers a clearer image of your budget yet additionally enhances your negotiating setting when making an offer.

Long-Term Wealth Building Strategies

Building long-lasting wide range through homeownership requires a calculated approach that exceeds just safeguarding a home loan. One reliable technique is to think about the recognition possibility of the building. Selecting homes in growing communities or locations with intended developments can cause substantial rises in property value over time.

Another essential facet is leveraging equity. As home mortgage settlements are made, homeowners build equity, which can be used for future financial investments. Making use of home equity financings or credit lines sensibly can supply funds for extra real estate investments or restorations that even more enhance home value.

Furthermore, keeping the property's problem and making calculated upgrades can considerably contribute to long-lasting riches. When it comes time to market., simple improvements like energy-efficient devices or modernized bathrooms can generate high returns.

Last but not least, understanding tax benefits linked with homeownership, such as home loan interest deductions, useful source can boost economic results. By making best use of these benefits and adopting a positive investment frame of mind, home owners can cultivate a durable profile that fosters lasting riches and security. Ultimately, a well-shaped strategy that focuses on both residential property option and equity management is essential for sustainable riches structure through realty.

Preserving Financial Safety And Security

Furthermore, fixed-rate home loans provide predictable month-to-month settlements, allowing much better budgeting and economic planning. This predictability safeguards homeowners from the variations of rental markets, which can cause unexpected increases in housing prices. It is vital, however, to ensure that home loan repayments remain convenient within the broader context of one's economic landscape.

Furthermore, responsible homeownership entails routine maintenance and renovations, which secure residential property value and boost general safety and security. Home owners must likewise take into consideration diversifying Visit Website their economic portfolios, making certain that their investments are not solely linked to realty. By integrating homeownership with other monetary tools, individuals can develop a balanced strategy that reduces threats and improves general economic security. Eventually, keeping financial safety and security through homeownership needs a positive and informed approach that stresses careful planning and ongoing diligence.

Final Thought

In final thought, effectively navigating the home car loans landscape necessitates an extensive understanding of various lending types and an extensive assessment of individual monetary situations. Implementing critical borrowing techniques assists in long-lasting wide range build-up and safeguards monetary stability.

Browsing the complexities of home lendings is essential for any individual looking to construct wealth and make certain economic safety and security.Evaluating your financial scenario is a critical step in the home financing process, as it lays the structure for making notified borrowing choices.Homeownership not just serves as a lorry for long-lasting wealth structure yet likewise plays a significant function in keeping monetary safety and security. By combining homeownership with other monetary instruments, people can produce a well balanced technique that mitigates dangers and boosts general monetary stability.In final thought, properly navigating the home finances landscape demands an extensive understanding of numerous car loan kinds and a thorough analysis of individual monetary scenarios.

Report this page